How To Reduce Your Business Risk

Running your own business can be rewarding. You get to follow your passion, choose who you work with and there is potential for higher financial returns. Being a business owner sounds irresistible with the flexibility, independence and freedom, however, there is a catch. There are risks and pressure.

Apart from the financial risk of running your own business there are side effects including long hours, isolation and the boundaries

between work and family life become blurred. This cocktail of issues can impact on your mental health. As accountants, our client

brief includes helping you reduce risk and there are several strategies to consider that can help reduce risk in your business.

FAILING TO PLAN IS PLANNING TO FAIL

Before

you launch your business, you need to put together a business plan. This should be your blueprint for the future of the business and

include an analysis of the current market, your competitors and document your marketing plan. You also need to crunch the numbers and

produce a forecast profit and loss for your first year of trading to make sure the business is viable. If it doesn’t pass the financial

test it’s back to the drawing board to rework your pricing, marketing, suppliers or product offering.

Before

you launch your business, you need to put together a business plan. This should be your blueprint for the future of the business and

include an analysis of the current market, your competitors and document your marketing plan. You also need to crunch the numbers and

produce a forecast profit and loss for your first year of trading to make sure the business is viable. If it doesn’t pass the financial

test it’s back to the drawing board to rework your pricing, marketing, suppliers or product offering.

You also need a cash flow budget which requires you to make assumptions about your prices, projected sales and costs. While it’s never easy to forecast your future sales with a high degree of accuracy, you need to consider putting several budgets together that incorporate your best- and worst-case scenarios. Given a lack of cash is the number one reason behind business failures in this country your cash flow budget is critical because it will help identify if you’re likely to need finance, how much you’ll need and when you’ll need the injection of funds. In business, forewarned is forearmed and if you need to apply to the bank for finance you need to do it well in advance of your funds drying up.

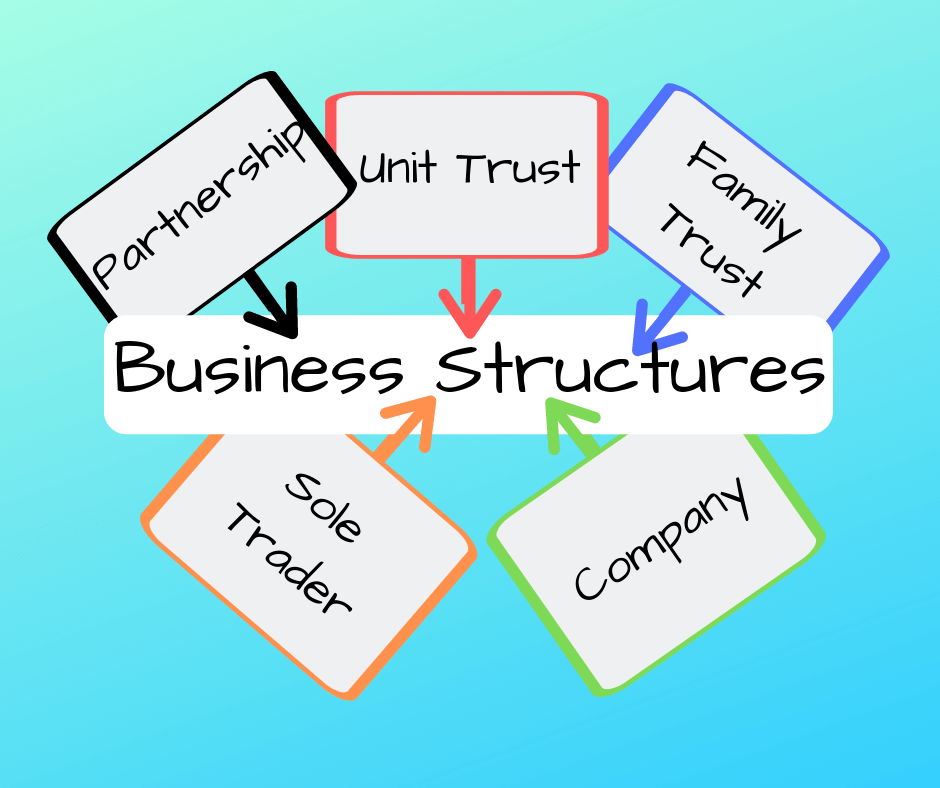

BUSINESS

STRUCTURE

BUSINESS

STRUCTURE

Your business structure can reduce risk by providing asset protection in the event the business turns sour. If you operate as a sole trader

or partnership, you are personally liable for the debts of the business and your personal assets can be used to recover the debts of the

business.

By contrast, a company structure is a separate legal entity that can sue and be sued. It can potentially protect your personal assets from the activities of the business. However, as a company director you are still exposed in the event you offer a personal guarantee to secure a bank loan. As such, you could be personally liable for the repayment of a business loan in the event the business can’t service the debt. Also, as a company director, you may also face personal liability for company debts if the business is declared bankrupt or incurs losses caused by a breach of director duties.

Whenever

we provide advice on business structures we always take into consideration tax minimisation, asset protection, the likely admission of new

partners in the future and entitlement to discount capital gains tax concessions. As a consequence, the choice of business structure is

often a compromise based on the relative importance of each of these issues. We urge you to consult with us before you make this

significant decision.

Whenever

we provide advice on business structures we always take into consideration tax minimisation, asset protection, the likely admission of new

partners in the future and entitlement to discount capital gains tax concessions. As a consequence, the choice of business structure is

often a compromise based on the relative importance of each of these issues. We urge you to consult with us before you make this

significant decision.

ASSET OWNERSHIP

As a director of a company, to reduce risk, it may be prudent to not own key assets in your own name. For example, ownership of your

principal place of residence and other significant personal assets can be owned by those not associated with the business including your

spouse.

INSURANCES

Without the right insurances your business could be at risk. All the time and money you invested into your business could be lost due to a

single event like a fire, storm or burglary.

Insuring against risks that could have a significant impact on your business is an essential part of running a business. While insurance can seem like another cost in a long line of expenses, if your business is uninsured (or under insured) you may never recover from a natural disaster, burglary, act of vandalism, fire or storm.

You need to address your specific business insurance needs and expect the unexpected. It’s also important to make sure your insurance coverage doesn’t fall behind as your business grows or diversifies. The size and nature of your business will generally determine the type of insurance coverage you need and some insurances you might need include:

- Public liability insurance to cover customers, clients and visitors

- Cover for building and contents, equipment, stock, furnishings and fixtures

- Professional indemnity insurance if your business is in a service industry - cover is usually purchased by professionals such as IT consultants, surveyors, accountants, solicitors etc. This cover will protect your legal liability to third parties arising from your (or your employees) professional negligence/wrongful advice.

- Product insurance if your business is in a manufacturing industry

- Motor vehicle insurance if your vehicle is used for business purposes

- Personal injury and/or income protection, particularly if WorkCover is not applicable to your business

QUALITY RECORD KEEPING

Given a lot of business failures are due to poor management, up to date, accurate records are important because they let you make informed business decisions. In business you’ll have to make snap buying and selling decisions and if you don’t have current data you are not in control. As they say, knowledge is power.

Modern software can provide an incredible amount of data about your business’ performance, your suppliers and your customers. As mentioned, poor cash flow is the biggest business killer and you need to know your debtors and the number of days they are outstanding because a slowdown in payment could lead to a cash-flow crunch. Similarly, you need to carefully monitor your accounts payable.

Good record keeping ensures that your financials and tax returns are prepared on cue and lodged with the Tax Office and other interested

parties like your bank if you have finance in place. Not only that, with financials at your fingertips, together with your accountant you

can do some tax planning that could save you money and defer your tax liability. Business intelligence software can also give you access to

data to help you identify trends that may create risks and opportunities in your market.

SUMMARY

Implementing standard operating procedures in your business can eliminate potential sources of risk and product risk can be managed by

introducing quality assurance programs. Conservative financial management can also reduce risk while backing up your electronic data

reduces the risk of losing your data files. Of course, appointing competent staff can also reduce business risk and instituting a

succession plan can protect the future of the business.

.png) Clearly, risk is part of running a business, however, there are a number of strategies that can help reduce risk. Every industry and

business is different but the items listed above serve as a useful checklist. If you’re looking to start a business our ‘New Business

Starter Kit’ addresses a number of these issues and it also includes templates for a business plan, cash flow budget and profit and loss

statement. You can download a copy from the right-hand side of any page on our website.

Clearly, risk is part of running a business, however, there are a number of strategies that can help reduce risk. Every industry and

business is different but the items listed above serve as a useful checklist. If you’re looking to start a business our ‘New Business

Starter Kit’ addresses a number of these issues and it also includes templates for a business plan, cash flow budget and profit and loss

statement. You can download a copy from the right-hand side of any page on our website.

Arrange Your FREE

No-Obligation Meeting

Either phone us on (03) 5744 3861 or complete the form below

Download now and get your

business off to a flying start!

ABN 64 155 907 681 AFSL Number 430062.

O'Bryan & O'Donnell (ABN 52 138 942 258) are Corporate Authorised Representatives (Number 001299902) of SMSF Advisors Network Pty Ltd.